In The Outsiders, an outstanding book about revolutionary corporate leadership, William Thorndike profiles eight unconventional CEO’s who re-wrote the rules of capital allocation and, in so doing, delivered phenomenal returns to shareholders during their tenure.

These eight CEO’s, including the likes of Henry Singleton of Teledyne and Tom Murphy of Capital Cities/ABC, believed in a laser-like focus on capital efficiency as the key to consistent, growing profits. While many CEOs pursue a “growth at any cost” mindset and believe that “bigger” is always better, these eight select CEOs saw things differently. As Tom Murphy said, “The goal is not to have the longest train, but to arrive at the station first using the least fuel.”

Thorndike recognized that, in terms of assessing CEO performance, it’s not absolute performance that matters so much as performance relative to one’s peers and the broader stock market. It’s one thing to deliver strong performance when the general economic and market environment is favorable, quite another to do so when facing economic headwinds. In other words, context matters.

“The goal is not to have the longest train, but to arrive at the station first using the least fuel.”

Tom Murphy, Capital Cities/ABC

Viewed in that light, the results of this select group have been remarkable. How did they do? Henry Singleton delivered annual compound returns of 20.4% during his tenure, while his peer group managed only 11% per annum. Put another way, a dollar invested with Singleton would have grown to nearly $180 by the time he retired, compared to only $15 if invested in the S&P 500.

Likewise Tom Murphy of Capital Cities/ABC delivered similarly phenomenal returns, compounding at 19.9% over a 29 year stretch, easily outdistancing the 10.1% compound return for the S&P 500 and 13.2% for media companies during that same time period.

The track record of Henry Singleton and Tom Murphy typified those of the entire group of “Outsiders”. Over a 25 year period, their aggregate performance was approximately 30 times that of the S&P 500, and 9 times that of their peer group. In addition to Singleton and Murphy, Thorndike’s select group of CEO’s includes John Malone of TCI, Richard Smith of General Cinema, Bill Anders of General Dynamics, Katherine Graham of the Washington Post Co., Bill Stiritz of Ralston Purina, and Warren Buffett of Berkshire Hathaway.

With those successful track records, an idea presents itself: why not create a portfolio of publicly-traded businesses that deliver ever-growing profits while utilizing capital as efficiently as possible? We call it the Capital Misers portfolio. We’ll get to the methodology below, but first let’s dive into the numbers.

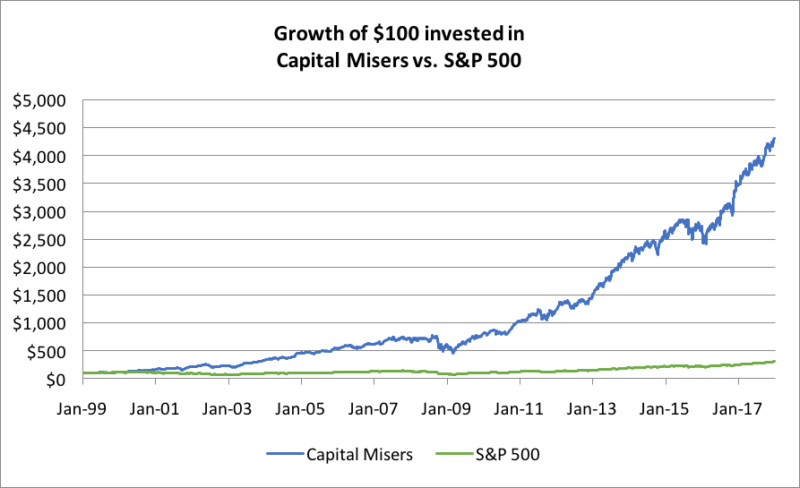

The long-term results of this strategy are outstanding across all metrics including absolute and relative performance, consistency and risk-management. Over a 19-year period from 1999 through 2017, the Capital Misers portfolio would have significantly outperformed the S&P 500 and done so with less downside exposure during the two major bear markets of 2000-2002 and 2008-2009.

Just how good was Capital Misers? A portfolio of 20 such stocks, rebalanced annually, would have compounded at 21.9% annually over that 19-year stretch vs. 6.09% annually for the S&P 500 . Furthermore, the Capital Misers portfolio delivered this performance with less permanent risk to capital, experiencing a maximum drawdown of 42.4% vs. 54.6% for the broader market. This model portfolio would have lost money in just one year (2008), and outperformed the broader market in all years but two (2006 and 2017). The Sharpe Ratio, a measure of risk-adjusted returns, was 1.15 for the Capital Misers portfolio vs. 0.35 for the S&P 500 during that time period.

Source: S&P Compustat

Risk Metrics:

| Total

Return |

Annualized

Return |

Max

Drawdown |

Sharpe

Ratio |

Sortino

Ratio |

Standard

Deviation |

|

| Capital Misers | 4,205.77% | 21.91% | -42.24% | 1.15 | 1.60 | 16.97% |

| S&P 500 | 207.51% | 6.09% | -54.62% | 0.35 | 0.46 | 14.56% |

Annual performance:

| Year | Capital Misers | S&P 500 | Relative Performance |

| 1999 | 36.39 | 21.11 | +15.28 |

| 2000 | 36.3 | -9.11 | +45.41 |

| 2001 | 39.32 | -11.98 | +51.30 |

| 2002 | -0.08 | -22.27 | +22.19 |

| 2003 | 43.52 | 28.72 | +14.80 |

| 2004 | 46.33 | 10.82 | +35.51 |

| 2005 | 6.07 | 4.79 | +1.28 |

| 2006 | 15.53 | 15.74 | -0.21 |

| 2007 | 16.9 | 5.46 | +11.44 |

| 2008 | -17.42 | -37.22 | +19.80 |

| 2009 | 30.28 | 27.11 | +3.17 |

| 2010 | 19.32 | 14.87 | +4.45 |

| 2011 | 12.64 | 2.07 | +10.57 |

| 2012 | 23.77 | 15.88 | +7.89 |

| 2013 | 51.71 | 32.43 | +19.28 |

| 2014 | 24.44 | 13.81 | +10.63 |

| 2015 | 3.13 | 1.31 | +1.82 |

| 2016 | 34.36 | 11.93 | +22.43 |

| 2017 | 18.12 | 21.93 |

-3.81 |

Capital Misers Portfolio Methodology

The portfolio is constructed using the following rules, incorporating elements of capital efficiency, margin of safety and earnings growth:

- Capital Expenditures as a % of Sales are less than ⅔ that of the industry peer group

- The 5-Year Return on Investment is greater than 10% and Gross Margins are greater than 15%

- Enterprise Value / Free Cash Flow is less than 15.

- Earnings per share are growing at least 12% per year over the prior 3 years.

- The most recent Current Ratio (current assets divided by current liabilities) is at least 95% that of the prior year’s Current Ratio, or shares outstanding have been reduced by at least 5% over the prior year.

Subject to the above criteria, we select the top 20 Capital Misers by EPS growth.

Rebalance Methodology

- Stocks are equal-weighted

- Rebalance on January 1 of each year

- Stocks that are not renewed are sold and the proceeds are distributed equally among remaining portfolio positions.

- Dividends are reinvested

- In the event of an acquisition, the proceeds are reinvested. In the event of a spin-off, the shares are sold and reinvested in the parent.

Current Portfolio

Here’s what the portfolio looks like for 2018:

| Ticker | Name | Mkt Cap $ (000) | Sector |

| USNA | USANA Health Sciences Inc | 1,773 | Staples |

| SCS | Steelcase Inc. | 1,763 | Industrial |

| MO | Altria Group Inc | 136,366 | Staples |

| AVY | Avery Dennison Corp | 10,117 | Materials |

| MMS | MAXIMUS Inc. | 4,663 | Technology |

| WBA | Walgreens Boots Alliance Inc | 74,352 | Staples |

| WOR | Worthington Industries Inc. | 2,677 | Materials |

| NTRI | NutriSystem Inc | 1,580 | Discretionary |

| AMAT | Applied Materials Inc. | 54,187 | Technology |

| ICLR | Icon PLC | 6,073 | Healthcare |

| AYI | Acuity Brands Inc. | 7,369 | Industrials |

| CCMP | Cabot Microelectronics Corp | 2,379 | Technology |

| EVR | Evercore Inc | 3,474 | Financial |

| EGOV | NIC Inc | 1,100 | Technology |

| MIDD | Middleby Corp (The) | 7,545 | Industrial |

| TXN | Texas Instruments Inc | 103,015 | Technology |

| MAN | ManpowerGroup Inc | 8,355 | Industrial |

| BBY | Best Buy Co Inc | 20,267 | Discretionary |

| PATK | Patrick Industries Inc | 1,752 | Industrial |

| CRUS | Cirrus Logic Inc. | 3,302 | Technology |

We will provide ongoing performance updates for the Capital Misers Portfolio here on our Insights page.

Source (notes 1,2,3): The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success. William Thorndike, 2012.